Summary/Reflections

Founders' deep ties to their customers drive successful VSaaS businesses

We’ve seen time and time again, the best positioned to disrupt in VSaaS tend to be industry veterans

Navigating small TAM can be crucial to success; raising of funding rounds pre-maturity can hinder success unless focused on M&A or establishing new products

Add-on products drive growth, and successful integration can be established through M&A

Down-market focus is not a priority, only focus on quality customers

Economic resilience through non-discretionary demand: Their end-users (the trades) are fundamentally non-discretionary, fueling rapid growth even through down markets

Overview and Origins

Overview

ServiceTitan recently filed a much-anticipated S-1 in preparation for IPO. As of December 3, 2024, they’ve prepared to seek a valuation of up to $5.16B offering 8.8 shares priced between $52 and $57

Though much analysis has been done on their S-1 from great thinkers such as Meritech Capital and Mostly Metrics, I thought it would be much more interesting to look at the IPO from a product-based perspective. How does their market structure and origin story influence their product expansion and strategy?

Origins

ServiceTitan was founded in 2012 by Ara Mahdessian and Vahe Kuzoyan, though they began thinking about the concept as early as 2007. After meeting over a Ski trip, Ara and Vahe, both children of Armenian immigrants who were home-service contractors in building and plumbing who frequently ran into issues with the logistics of running their companies, became inspired to work on a summer project together, which became ServiceTitan.

Sidenote: their personal connection to the issue they were solving continued to be a crucial part of their identity, as later hires such as Thomas Howard, their VP of Customer Success came from the industry, some of which also happened to be customers of ServiceTitams themselves

What started out as a simple desktop program quickly became a cloud-based platform with a whole suite of products and services.

Market Opportunity: How Market Strategy Enables Product Expansion

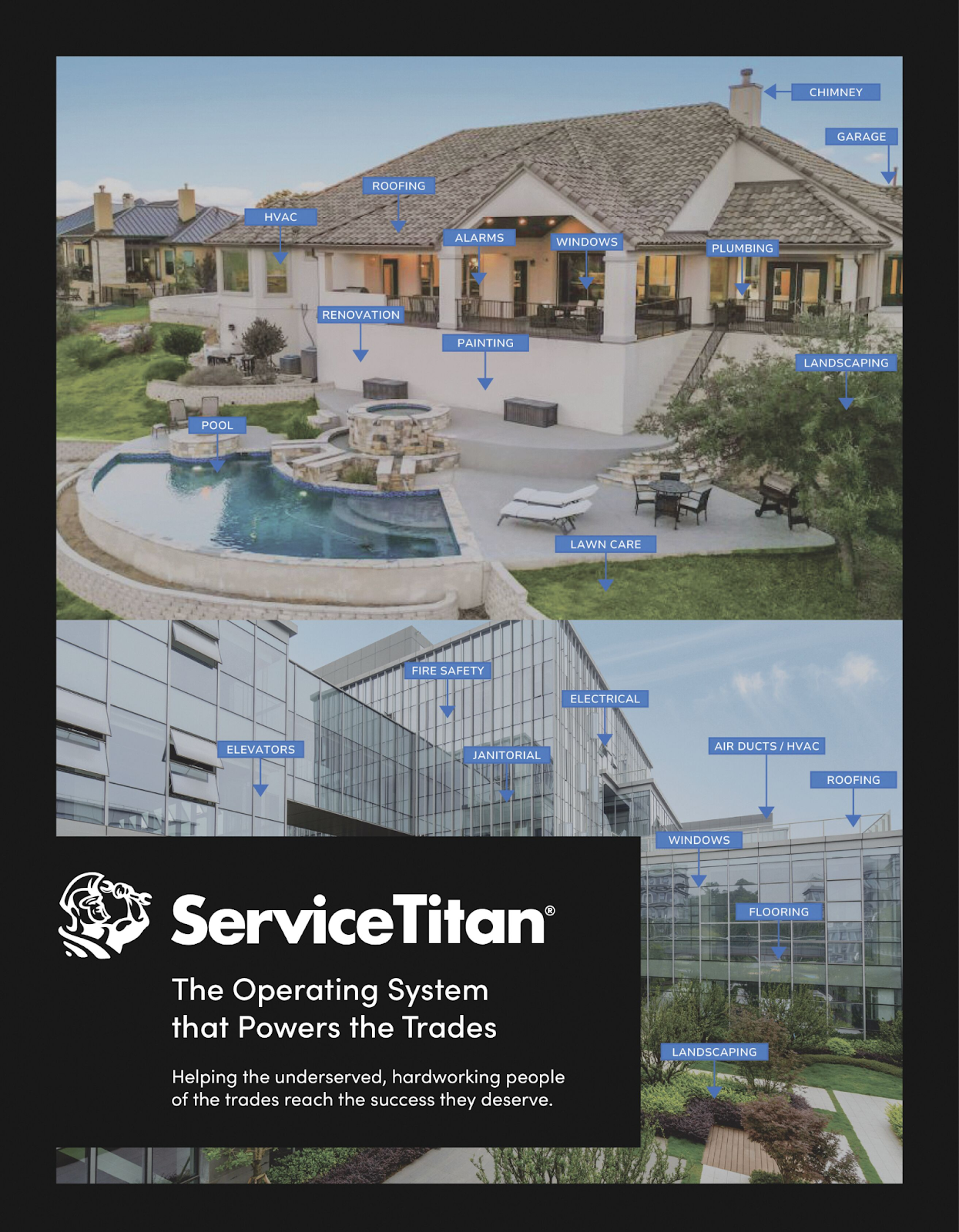

ServiceTitan launched its core product in 2012, a single-product cloud-based tool that enabled scheduling and dispatching software specific to one trade: residential-focused plumbing companies.

In other words, they created a venture-backed business by initially focusing on plumbing companies that only service homes, not commercial buildings. And to get even more specific, they started their launch by focusing only on residential plumbing companies that specialize in service and replacement work.

So, if your toilet's clogged, that's the plumber we would sell to, but if you're building a new house from the ground up, the plumber that built the plumbing infrastructure was not our customer1

And jumping back to 2012, selling vertical software was actually a unique strategy: the most popular approach was the build software and try to sell it to everyone. Some of the winning startups of the 2012s2:

(1) Snowflake / led by Sutter Hill / $57bn val

(2) Datadog / led by Index / $53bn val

(3) Reddit / led by Initialized / $25bn val

(4) Stripe / led by Sequoia / >$5bn val

(5) Github / led by a16z / acq. for >$5bn

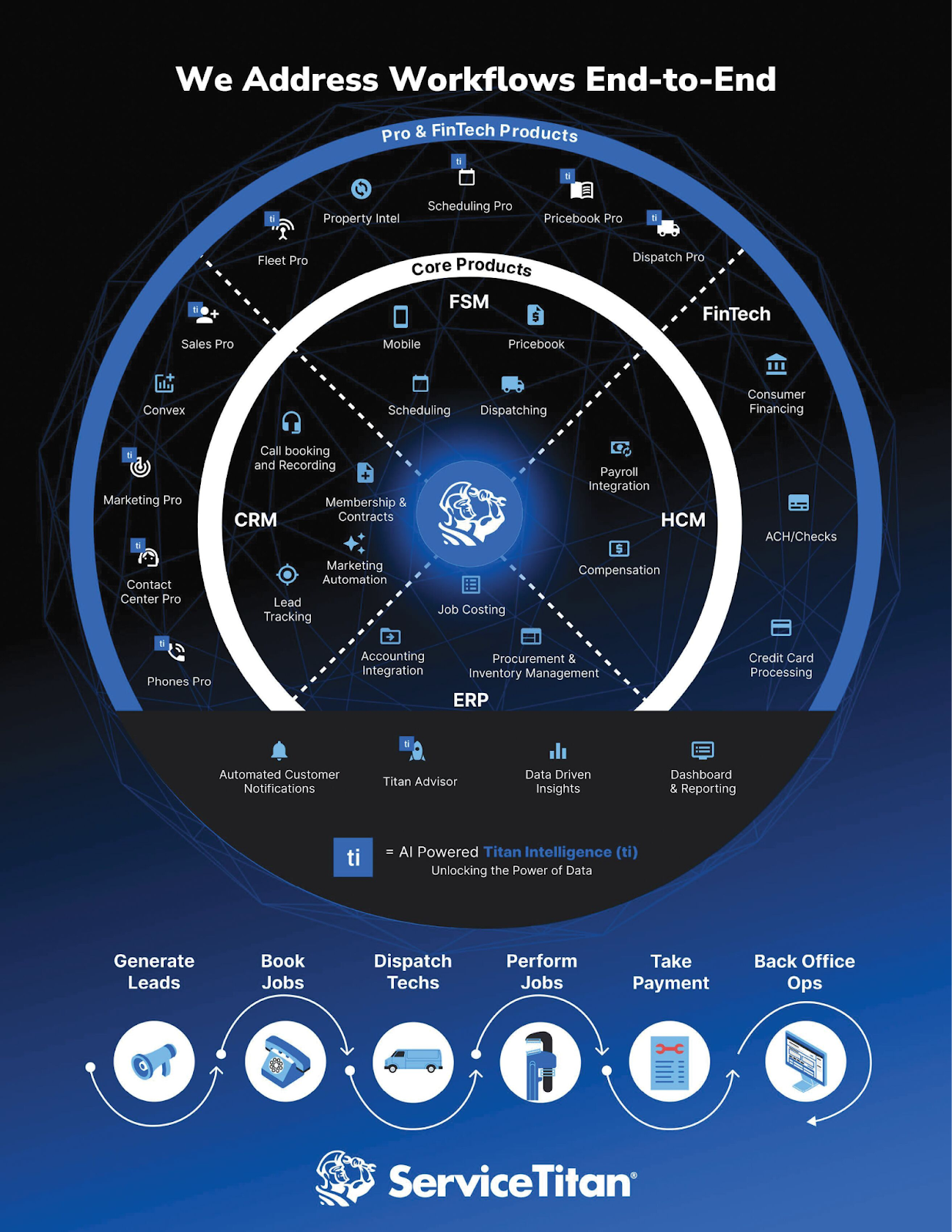

ServiceTitan felt differentiated: you can build something that is okay for everybody but is not amazing for anybody. They felt that on the extreme end, a targeted product could be a differentiator. Using this strategy, they quickly developed “control points” in VSaaS tech stacks, where key features such as:

Automated Scheduling: Optimizing technician timesheets and dispatch routes to reduce costs and increase job volume.

Integrated Payments: Streamlined invoicing and payment collections to get cash in faster.

CRM: Keep track of customer purchases and property details.

allowed them to gain significant workflow and data gravity. In addition, the executive-focused nature of their product (CRM, scheduling of lower-level workers, payments), allowed them significant account gravity, where their biggest advocate would typically be executives of larger contracting firms.

There was one issue: there are only so many residential plumbing companies that specialize in service and replacement work worldwide, and the average contract size is far from the venture scale.

So how did ServiceTitan operate? Retrospectively, they followed Tidemark Capital’s market structure strategy for Small TAM businesses to a tee.

A Lesson on Operating in a Small TAM

As Dave Yuan states3:

If you are in a small TAM, my advice as an investor may shock you: raise less money. Your best fundraiser is your customers … Expanding is not only about increasing your ARPU and making the merchant’s life easier. It is also about looking for expansion opportunities that help grow the TAM.

They raised their series A fairly late (2015), and continued to be fairly conservative until they truly achieved scale (~2017). However, after reaching maturity, they haven’t been shy about raising to fuel expansion in a winner-take-most market, raising Series G and H in 2021 and 2022 respectively to fuel several acquisitions, including:"

Aspire Software (June 30, 2021): A company specializing in software for landscapers.

ServicePro (February 2, 2021): A company specializing in software for pest control and lawn care contractors.

FieldRoutes (January 4, 2022): A provider of field service management solutions.

Schedule Engine (June 28, 2022): A company offering online booking services for home and commercial services.

Convex Labs (April 2, 2024): A firm specializing in sales enablement solutions.

Back to 2012… instead of focusing on increasing their ARPU and making the merchant’s life easier, they also looked for expansion opportunities that helped grow TAM.

Once they were able to deliver incredible ROI with residential plumbing and had customers who loved the product, they methodically extended into the next customer segment, which was HVAC. HVAC was an industry with 80-90% of the same needs, which led them to successfully deliver there and use the same playbook.

Soon after HVAC, they quickly went to electrical, and soon enough were in 10 different trades. They also began expanding into lighter-weight construction-focused companies–many of which they are just starting to tackle as well.

Alongside simple vertical expansion, they also employed clever sales tactics. As stated by BVP4:

ServiceTitan, the vertical software company for commercial and residential trades, had a strategy at this stage to first win market share, and then in the future to expand usage of its product suite across its customer base. To accomplish this, company leadership wanted the sales team to prioritize new logo acquisition. The company created a specialized Account Management function dedicated to expansion opportunities that freed up sales rep resources to focus on landing new opportunities. Whereas in the past one person handled both new logo acquisition and expansion, now the functions were formally separated and delineated.

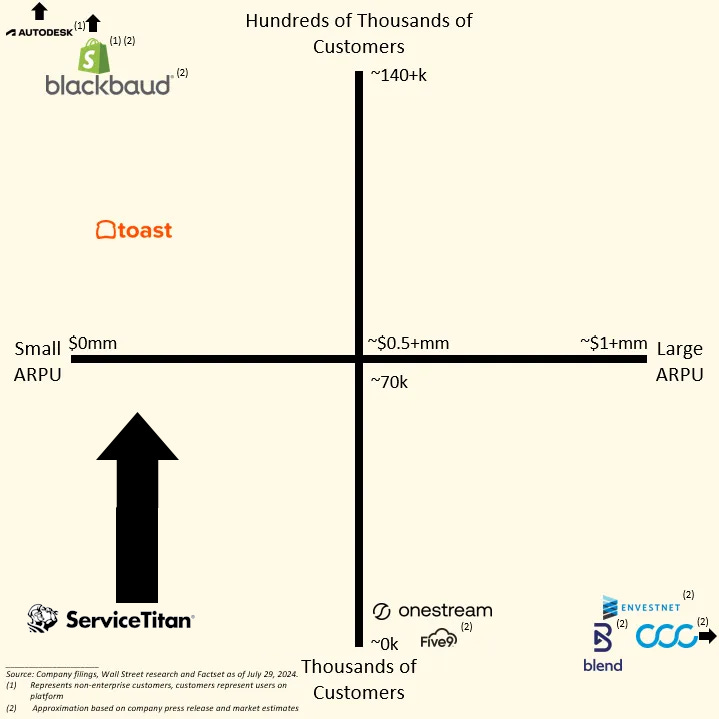

ServiceTitan was quickly able to grow its TAM to go from the dreaded bottom left corner of ARPU x Customers to reach a spot with acceptable TAM and eventually raise an $18 million Series A funding round led by Bessemer Venture Partners in 2015.

Today, they boast a diverse proposed TAM of $650B broken down into:

Residential service: $180B

Commercial service: $260B

Residential construction: $110B

Commercial construction: $100B

Product Expansion

Beyond just TAM/industry expansion they also sought out product expansion. Though just originally focused on medium capability across every function, and the marginal ~10% of product development needed to tailor products towards more specific trades, they quickly learned that customers also wanted a very high-end professional level of capabilities in their areas. They quickly expanded to a ‘pro’ product, which now includes everything up to Marketing Pro, Scheduling Pro, Dispatch Pro, Pricebook Pro, etc.

However, important to keep in mind is that while operating in this small TAM, sure they realized additional cross-selling opportunities into tiered versions of their products, but they focused on the core competencies of their vertical software business and remained, effectively, single-product.

Today, ServiceTitan claims that they only capture ~1% of Gross Transaction Value on the platform as top-line revenue, projecting an overall take rate of ~2% assuming additional product penetration. As calculated by Meritech:

By applying the ~2% against the $650B of serviceable industry spend, ServiceTitan believes their total revenue opportunity is ~$13B. Based on the GTV generated by customers during the 12 months ended July 31, 2024, ServiceTitan estimates they have <10% penetration in the ~$650 billion serviceable industry spend.5

Alignment of Business Model With Growth

ServiceTitan was also uniquely positioned to profit significantly from the growth of its end-user. Unlike horizontal software, where the growth of the end-user often leads to the development of in-house replacements, ServiceTitan often found that as their software helped their customers grow significantly, they also saw their end users higher more technicians, thus adding more ServiceTian licenses. It’s the classic success story of a seat-based pricing model here.

VSaaS Network Effects

In addition, ServiceTitan leans into the light network effects often appreciated by VSaaS vendors–where employees become familiar with a system, and when they switch jobs/start new businesses they will bring along the tools that are familiar–by offering playbooks on contracting business self-starting and encouraging to leverage ServiceTitan as a life-long partner in their trades journey.

They’ve also garnered the largest community of contractors in a Facebook group. And this leads to significant benefits, including community-driven benchmarking:

Every day we have one contractor after another posting their ServiceTitan dashboard in that group. They’re comparing everything—revenue growth, average ticket, close rate, technician performance. It happens organically, but yes, we do want to make that available to customers in the app.

Financial Benchmarking

It wouldn’t be an S-1 Breakdown without some interesting financials (Thanks to Meritech & Mostly Metrics for the number crunching):

Net Dollar Retention Rate (NDR): +110%

Gross Dollar Retention (GDR): +95%

Top-of-the-line VSaaS businesses are still dominating NDR, as well as GDR—successful Vertical SaaS businesses typically enjoy outlier-level GDR Numbers

Customers: ~8000

Medium sized end-user base has forced them to not only expand their TAM with additional verticals, but product growth to sustain growth

Top 10 Customers Contribution: ~10% of total revenue

Low customer concentration risk; a factor of their sticky/non-discretionary end-user

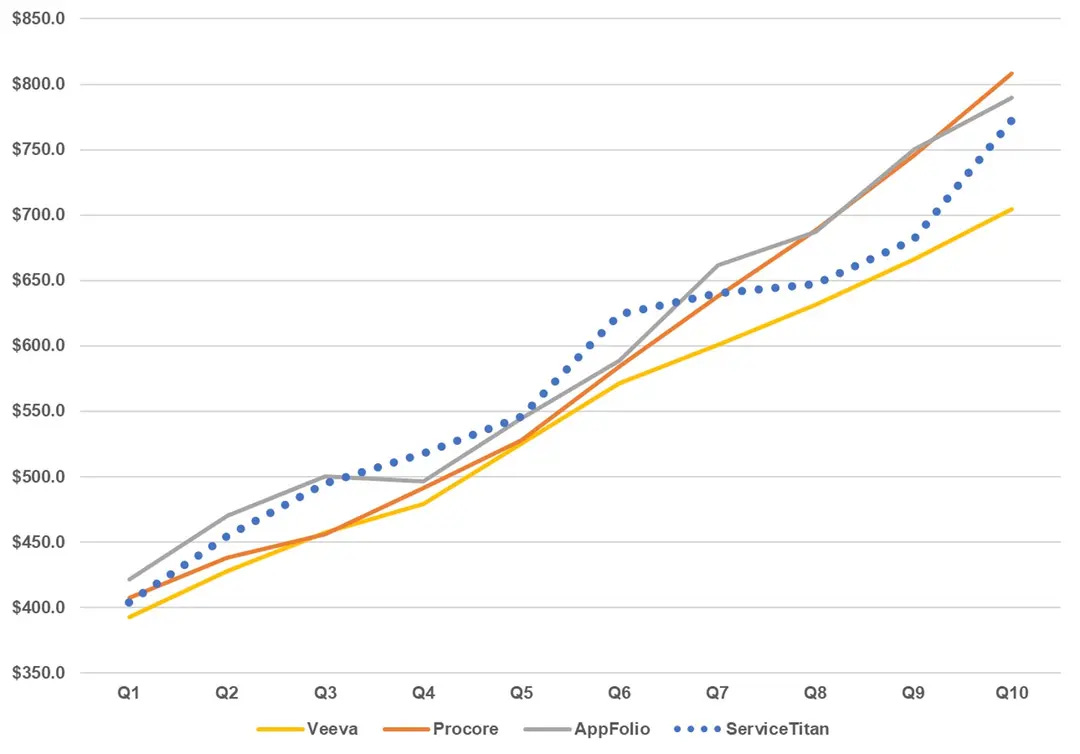

Revenue growth rate: 31.1% YoY; ARR Growth Rate, 24%

This puts them far above the median 15% topline growth in 2024 amongst public SaaS companies. It also plays into the broader success of vertical saas, highlighted by OneStream’s successful IPO earlier in the year. This is a broader sign across the software industry, given:

Amongst All Companies, Vertical Software Companies experienced far Greater Topline Growth Than Horizontal Software6

Median Growth Vertical (45%) vs Horizontal (28%)

Top Quartile Growth (100%) vs Horizontal (56%)

ServiceTitan’s YoY growth rate of 31.1% puts them at competitive levels with VSaaS vendors at $5-20M ARR (37%) and far above Horizontal SaaS vendors at $5-20M ARR (20%)–ServiceTitan’s exceptional growth rate coupled with the scale of VSV platform demonstrates the success of vertical saas

They also follow similar revenue growth projections to other public vertical SaaS businesses (despite different expansion strategies):

Conclusion

I’m excited about ServiceTitan’s continued growth opportunities post-IPO:

As a VSaaS leader with significant workflow/data gravity amongst various verticals with growth opportunities into marketplaces, and employee recruiting, amongst others, along with top-of-the-line financials, ServiceTitan is set to receive an IPO success, similar to another Vertical SaaS success story, OneStream

Proven success in market and vertical expansion give me hope for sustained top-line growth

I’m still a little skeptical about their ability to transition to profitability and their reliance on professional services–however as we’ve seen with other successful VSaaS businesses, many times a gravity-inducing product requires significant services-driven growth

Though none of this is set in stone, I’m excited to see ServiceTitan and OneStream continue to prove the venture-backability of Vertical SaaS and continue to improve lives for their end-users, oftentimes small businesses.

Thats All!

Hope you enjoyed my breakdown of ServiceTitan and the first post with my newly branded substack, Fundamentally. Stay tuned for future company breakdowns beyond just VSaaS.

I’m always open to discussions — feel free to reach out on LinkedIn or on X @Alson__C.

“What made ServiceTitan a Rocket Ship” https://allisonpickens.substack.com/p/what-made-servicetitan-a-rocket-ship&sa=D&source=docs&ust=1733287804648147&usg=AOvVaw1GuUvtn3ktZ-eqFBSqA4cp

via Cole Rotman on X: https://x.com/ColeRotman/status/1863422600611078568

“Market Structure Drives Strategy” https://www.tidemarkcap.com/post/market-structure-drives-strategy

“Scaling GTM From 25 to 50 Million ARR” https://www.bvp.com/atlas/scaling-gtm-from-25-to-50-million-arr

“ServiceTitan S-1 Breakdown” https://www.meritechcapital.com/blog/servicetitan-s-1-breakdown

“2024 SaaS Benchmarks” https://www.highalpha.com/2024-saas-benchmarks-report#download-report